Global cellular IoT connections surpassed 4 billion in 2024, driven by 5G and LTE Cat 1 bis

In short

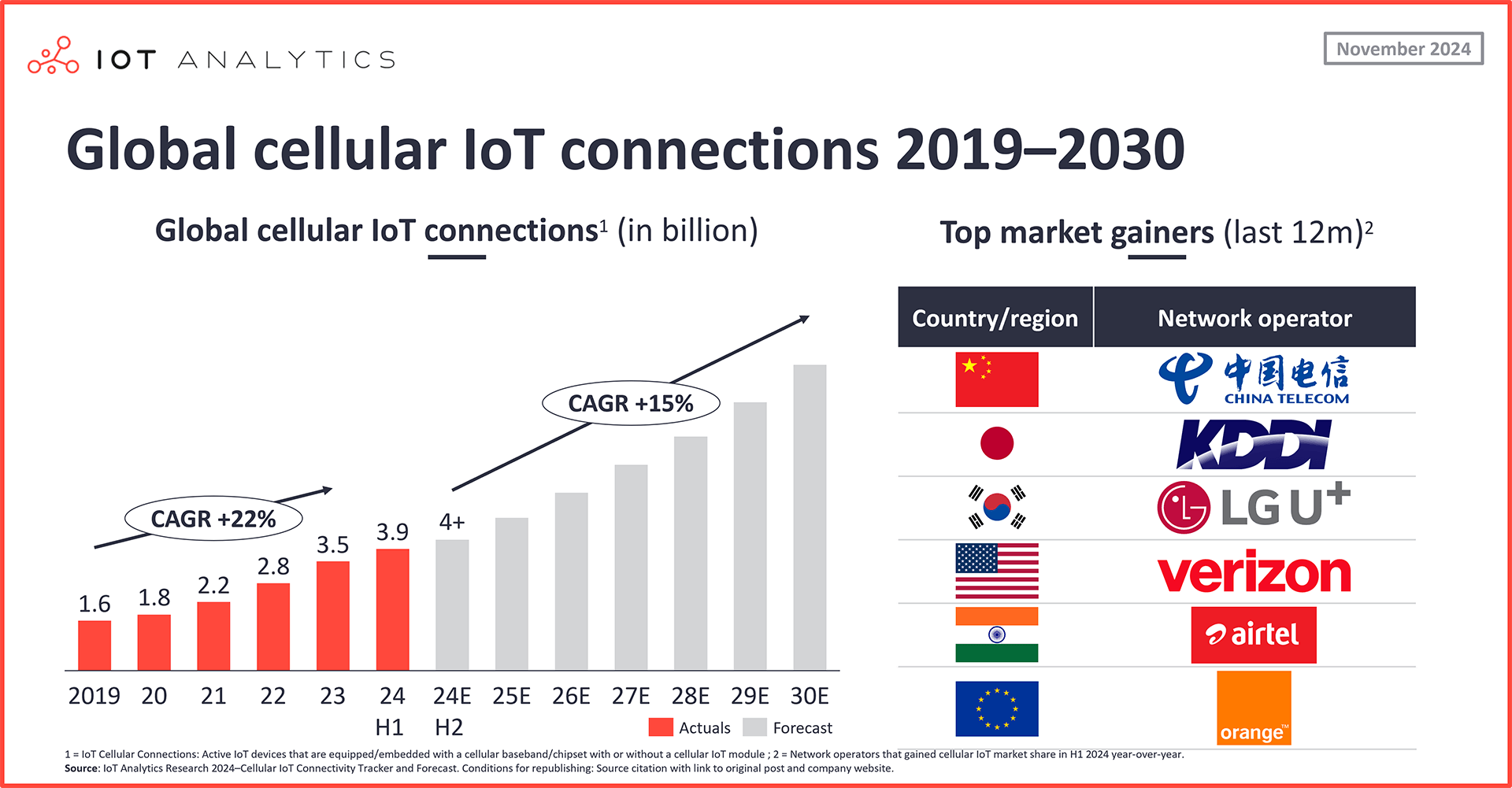

- Global cellular IoT connections reached 3.9 billion in H1 2024, according to IoT Analytics’ updated Global Cellular IoT Connectivity Tracker & Forecast.

- Based on ongoing tracking and analysis, cellular IoT connections have surpassed 4 billion as the end of 2024 approaches, representing approximately 22% of global overall IoT connections.

- Connections are expected to grow at a CAGR of 15% between 2024 and 2030, driven by LTE Cat 1 bis and 5G.

- Notable mobile operators that gained market share in H1 year-over-year include China Telecom, Airtel, KDDI, LG U+, Orange, and Verizon.

Why it matters

- For mobile operators: With cellular IoT connectivity gaining market share of the overall IoT connections worldwide and LTE Cat 1 bis and 5G driving growth, mobile operators should learn from successful peers.

- For chipset, module, and device producers: Cellular IoT connectivity is on the rise, and chipset, module, and device producers should consider their relationships with mobile operators to expand market reach and ensure smooth integration with new cellular IoT technologies.

Market update

Global cellular IoT connections reached 3.9 billion in the first half of 2024, according to IoT Analytics’ quarterly Global Cellular IoT Connectivity Tracker & Forecast (updated in November 2024), representing 20% growth YoY and 181% over the last 5 years. IoT Analytics’ ongoing analysis has found that as we approach the end of 2024, cellular IoT connections have surpassed 4 billion, representing approximately 22% of the projected 18.8 billion global IoT connections by the end of 2024 (more on this in the analyst take section toward the end).

LTE Cat 1 bis and 5G propel cellular IoT growth

The growth of LTE Cat 1 bis and 5G IoT underscores the evolving landscape of cellular IoT connectivity. LTE Cat 1 bis fills a crucial gap by balancing performance and power efficiency, especially in markets where LTE-M is unavailable. Moreover, LTE Cat 1 bis is now competing with LTE-M in some regions, such as Europe. Meanwhile, 5G IoT unlocks new possibilities for high-bandwidth, low-latency applications. Stakeholders in the IoT ecosystem have been implementing these technologies when developing future-proof solutions and strategies.

1. LTE Cat 1 bis

LTE Cat 1 bis has significantly contributed to cellular IoT growth, with connections increasing by 68% YoY in H1 2024. Based on 3GPP Release 13, LTE Cat 1 bis features a single antenna design optimized for low-power applications. Four key factors are fueling its adoption:

- Market demand: In China, the absence of LTE-M and the limitations of NB-IoT have accelerated the adoption of LTE Cat 1 bis. The country accounts for 85% of global LTE Cat 1 bis connections and experienced a 56% YoY growth in the first half of 2024.

- Balanced performance: LTE Cat 1 bis offers balanced high-speed capabilities—up to 10 Mbps downlink and 5 Mbps uplink—with low power consumption. It supports power-management features like Extended Discontinuous Reception (eDRX) and Power-Saving Mode (PSM), reducing power usage by allowing devices to sleep when not transmitting or receiving data. This makes it suitable for IoT applications requiring long-term operation without frequent battery replacements, such as smart metering, fleet management, healthcare devices, and payment solutions.

- Cost-effectiveness and simplified design: LTE Cat 1 bis’ single antenna design reduces hardware complexity and costs compared to the original LTE Cat 1, making it an attractive option for manufacturers and solution providers.

- Global coverage and futureproofing: LTE Cat 1 bis operates on existing LTE networks globally, offering extensive coverage. As 2G and 3G networks are decommissioned, it provides a seamless migration path that ensures longevity and continued support for IoT applications.

2. 5G IoT

5G IoT connections have also experienced substantial growth, driven by advancements in 3GPP Release 15 and beyond. These developments enhance capabilities for high-speed, low-latency applications critical for modern IoT solutions. Key reasons for 5G IoT growth include:

- Market demand: China’s significant investment in 5G infrastructure has created a robust ecosystem supporting widespread adoption. The availability of affordable 5G-compatible devices and modules has lowered barriers for industries to implement 5G IoT solutions. Analysis from the tracker shows that China holds approximately 80% of global 5G IoT connections and experienced 79% YoY growth in the first half of 2024.

- Enhanced performance and capabilities: 5G IoT offers ultra-low latency (as low as 1 ms) and high data rates (up to 20 Gbps), essential for applications requiring immediate responsiveness and high throughput. With the ability to support up to a million devices per square kilometer, 5G accommodates the escalating number of IoT devices.

- Two key applications. Fixed wireless access (FWA) and the automotive sector are driving 5G IoT growth in the following ways:

- FWA: FWA contributes 45% of global 5G IoT connections in the first half of 2024 by leveraging 5G networks to deliver high-speed internet access to homes and businesses, particularly in areas lacking fiber infrastructure. This approach offers a cost-effective alternative to traditional broadband services and expands connectivity in underserved regions.

- Automotive sector: The automotive sector, including transportation, supply chain, and logistics, accounted for 26% of global 5G IoT connections during the same period, propelled by connected vehicles. The industry is integrating 5G IoT to enhance real-time navigation, telematics, and infotainment. Additionally, 5G supports future technologies like Cellular Vehicle-to-Everything (C-V2X), enabling communication between vehicles, infrastructure, and other road users. Since vehicles produced now will remain in use for over a decade, integrating 5G ensures they stay compatible with emerging technologies throughout their lifespan.

The insights from this article are based on the Cellular IoT Connectivity Tracker and Forecast, an interactive dashboard and a structured database of worldwide cellular IoT connections from 2018 to Q2/2024, including a forecast for Q3/2024 to 2030.

Request a demo to experience a walk-through of the tracker via screen share and get your specific questions addressed.

Already a subscriber? View your tracker here →

Top cellular IoT market gainers in H1 2024

China: China Telecom

In H1 2024, China Telecom gained 5.3 percentage points in market share YoY in the Chinese market. Helping drive this growth was the company’s strategic focus on IoT-enabled solutions for sustainability and urban management. In August 2024, it reported some of its key initiatives, including:

- Green lighting: China Telecom offers a proprietary AI+IoT solution that promotes energy efficiency and carbon reduction by analyzing and predicting building traffic patterns. According to the company, this solution has saved over 6 million KWh of electricity and reduced over 1,700 tons of greenhouse gas emissions in 165 cities in 31 provinces.

- YiZhi city smart hub: By integrating its Xirang cloud computing and Xinghe AI platforms, China Telecom created the YiZhi smart city hub, a unified infrastructure to streamline urban applications, boosting smart city operations.

- Enhanced operations: China Telecom has deployed a proprietary IoT sensing cloud platform at the world’s largest single-building airport that supports over 20 applications, such as real-time coordination, decision-making, and passenger flow guidance, to enhance operational efficiency.

Japan: KDDI

KDDI gained 2.4 percentage points within the Japanese cellular IoT market, driven by strides in connected vehicles and AI-driven IoT solutions. Examples include:

- Connected vehicles: In February 2024, KDDI partnered with Sony Honda Mobility to enable global 5G connectivity for the AFEELA brand, enhancing user experiences in the CASE vehicle segment.

- Disaster preparedness: In March 2023, KDDI demonstrated telecommunications resilience with large-scale disaster drills, building trust in critical communication infrastructure.

- AI, IoT, and 5G integration: In June 2024, KDDI signed an agreement with 3 partners to commence planning and construction of what is expected to be the largest AI data center in Asia. KDDI plans to use the data center to support its WAKONX AI-driven digital transformation platform, which supports various industries, including mobility, logistics, and retail. Alongside KDDI in this venture are US-based server producer Super Micro Computer, Inc., Japan-based electronics vendor Sharp Corporation, and Japan-based software-as-a-service provider Datasection, Inc.

South Korea: LG U+

LG U+ gained 7.8 percentage points in the South Korean market YoY. Driving this growth is the company’s focus on IoT-enabled solutions and autonomous driving. Example solutions include:

- IoT-based safety solutions: In February 2023, LG U+ partnered with Korea-based waste disposal company Ecorbit to provide smart safety solutions at Ecorbit’s worksite. These solutions include IoT+AI-based safety equipment, AI forklifts, and driver behavior analysis.

- Autonomous vehicles: In April 2024, LG U+ collaborated with Rideflux to develop Level 4 autonomous driving solutions using AI and 5G. The number of LG U+’s connected vehicles grew 40% YoY in H1 2024.

United States: Verizon

Verizon gained 1.3 percentage points in the US cellular IoT market. This gain stems from advancements in IoT connectivity and global orchestration. Examples include:

- FWA and connected devices: In October 2024, Verizon reported an increase in its FWA user base and connected consumer devices like wearables and retail IoT devices.

- Global IoT orchestration: In July 2023, Verizon introduced its Global IoT Orchestration to enhance multinational cellular IoT connectivity. Its first international mobile network operator partners were Bell Canada and Norway-based Telenor.

- Telematics and connected vehicles: In February 2024, announced partnerships with automotive manufacturers Audi and AFEELA, offering private 5G and helping to drive connected car innovation.

India: Airtel

Airtel gained the most cellular IoT market share in India, largely due to its continued focus on the country’s fast-growing utility sector. Key initiatives include:

- Strategic partnerships: In December 2023, Airtel and IntelliSmart Infrastructure formed a strategic alliance. Airtel provides IntelliSmart with an end-to-end smart energy monitoring solution under a single service-level agreement (reducing complexity and deployment times) while also expanding the presence of its IoT solutions in various sectors.

- Smart metering initiatives: In January 2024, Airtel partnered with Adani Energy Solutions to connect over 20 million NB-IoT-powered smart meters across multiple states, enabling real-time energy management.

Europe: Orange

Orange gained the most market share in the European cellular IoT market by promoting IoT adoption and smart city solutions. Examples include:

- IoT Continuum kits: Since 2021, Orange and 3 partners have offered IoT Continuum kits to simplify IoT development and attract more enterprise customers. In September 2023, the partnership launched two IoT Continuum kits aimed at helping its customers begin and prove IoT projects. Orange’s partners for IoT Continuum are US-based IoT solutions provider Semtech, France-based electronic equipment design company LACROIX Group, and Switzerland-based semiconductor manufacturer STMicroelectronics.

- Smart water meter deployment: In March 2024, Orange partnered with Spain-based water management systems provider Hidroconta to digitalize over 100,000 smart water meters in Madrid, improving efficiency and reducing operational costs.

It is worth noting that Orange is successfully selling IoT connectivity outside of the European market. For example, in September 2023, the company signed an agreement with the King Abdullah Financial District Development & Management Company to design, build, and deploy an end-to-end smart city platform. The project aims to integrate and connect existing technologies within the district while leveraging AI and data analytics.

Analysts take on the cellular IoT market outlook

Double-digit growth projected for cellular IoT connections. After 20% growth YoY to 3.9 billion in H1 2024, ongoing market analysis shows that cellular IoT connections surpassed 4 billion by the end of Q3 2024 and are projected to reach 4.2 billion by the start of 2025. From there, the Global Cellular IoT Connectivity Tracker & Forecast forecasts connections to grow at a CAGR of 15% between 2024 and 2030.

India represents strong market opportunities. A key growth market to watch is India, where the government is undergoing a project to deploy 250 million smart meters by 2027. This initiative represents a $20 billion opportunity in energy management aimed at enhancing operational efficiency, enabling advanced data analytics, and optimizing resource utilization in the world’s most populated country. Large-scale projects such as this that adopt cellular IoT technologies will play a crucial role in modernizing energy.

5G IoT has been a game-changer for operators. On the technology side, 5G IoT is playing a crucial role in enabling higher bandwidth applications such as automotive connectivity, extending beyond connected vehicles to include vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) communications. Meanwhile, 5G FWA is also seeing rapid adoption, as it provides low-latency and high-speed internet similar to traditional broadband connectivity in areas lacking traditional broadband infrastructure, a positive for remote IoT connectivity needs.

5G Reduced Capability (RedCap) on the horizon. Looking ahead, 2025 will mark the first commercialization of 5G RedCap connections. This technology bridges the gap between full-scale 5G and existing LTE categories, like LTE Cat-4, with expectations of reaching Cat-1 levels with 5G Enhanced RedCap (5G eRedCap) that will be released in 3GPP Release 18. These advancements enhance device efficiency and cost-effectiveness, facilitating a smoother transition to next-generation connectivity and supporting a wide range of IoT applications, including mid-speed use cases like wearables and smart cameras.

Disclosure

Companies mentioned in this article—along with their products—are used as examples to showcase market developments. No company paid or received preferential treatment in this article, and it is at the discretion of the analyst to select which examples are used. IoT Analytics makes efforts to vary the companies and products mentioned to help shine attention to the numerous IoT and related technology market players.

It is worth noting that IoT Analytics may have commercial relationships with some companies mentioned in its articles, as some companies license IoT Analytics market research. However, for confidentiality, IoT Analytics cannot disclose individual relationships. Please contact compliance(at)iot-analytics.com for any questions or concerns on this front.

More information and further reading

Are you interested in learning more about the cellular IoT connectivity market?

Cellular IoT Connectivity Tracker and Forecast (Q4/2024 Update)

An interactive dashboard and a structured database of worldwide cellular IoT connections from 2018 to Q2/2024, including a forecast for Q3/2024 to 2030.

Request a demo to experience a walk-through of the tracker via screen share and get your specific questions addressed.

Already a subscriber? View your tracker here →

Related dashboard and trackers

You may also be interested in the following dashboards and trackers:

- Global Cellular IoT Connectivity Tracker & Forecast

- Global LPWAN Market Tracker and Forecast

- Global Cellular IoT Module and Chipset Market Tracker & Forecast

- Global IoT eSIM Modules and iSIM Chipsets

- Global IoT Enterprise Spending

Related publications

You may also be interested in the following reports:

- IoT Mobile Operator Pricing and Market Report 2024-2030

- 5G IoT & Private 5G Market Report 2024–2030

Related articles

You may also be interested in the following articles:

- The role of eSIM for IoT: Better security, simplified roaming, and easier provisioning—but only 33% of cellular IoT devices use it

- State of private 5G in 2024: Key growth trends, use cases, and forecast

- Benchmarking IoT mobile operator pricing: MNOs vs. MVNOs

Subscribe to our newsletter and follow us on LinkedIn and Twitter to stay up-to-date on the latest trends shaping the IoT markets. For complete enterprise IoT coverage with access to all of IoT Analytics’ paid content & reports including dedicated analyst time check out Enterprise subscription.

Leave a Comment